Tax Residency and Overseas Income

Moving Overseas? Living Overseas? Need Tax Advice?

Understanding your New Zealand tax residency is one of the most important factors in determining how much tax you need to pay and whether your overseas income must be declared to Inland Revenue (IRD).

Whether you’re moving overseas, returning to New Zealand, working remotely for a foreign employer or earning income from overseas investments, getting your tax residency status right is essential.

The rules can be complex, and incorrect assumptions can result in unexpected tax liabilities or missed reporting obligations.

At ABA Chartered Accountants, we provide international tax advice for individuals and businesses with overseas income, cross-border tax obligations and New Zealand tax residency matters.

Understanding Tax Residency & Overseas Income

We discuss:

- What makes you a New Zealand tax resident

- The 183-day rule explained

- Permanent place of abode rules

- When you stop being a New Zealand tax resident

- Whether you can be a tax resident of two countries

- What a Double Tax Agreement is

- How overseas income is taxed and what counts as foreign income

- IR1261 Overseas Income Summary

- Receiving money from overseas

- Working overseas while living in New Zealand

- Returning to New Zealand after living overseas

- Common scenarios where it’s best to seek international tax advice

- FAQs

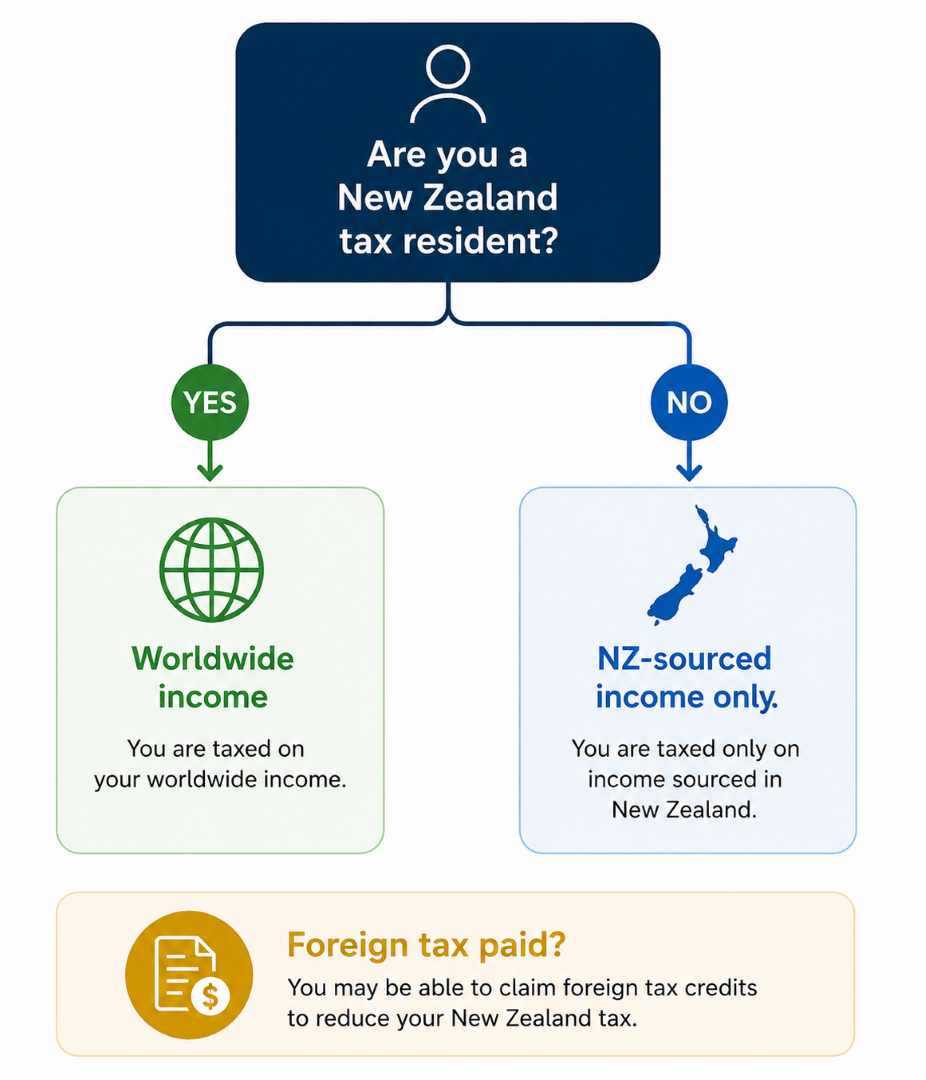

What is a New Zealand tax resident?

Your tax residency determines how New Zealand taxes your income.

If you are considered a New Zealand tax resident, you are generally required to declare your worldwide income, including income earned overseas.

If you are a non-resident for tax purposes, you will generally only pay New Zealand tax on income sourced within New Zealand.

It’s important to understand that tax residency is different from immigration or citizenship status.

You can be:

- A New Zealand citizen who is no longer a tax resident

- A visa holder who becomes a New Zealand tax resident

- A tax resident of more than one country at the same time

How does the IRD determine tax residency?

In New Zealand, a person’s liability for income tax depends on that person’s residency status.

Inland Revenue looks at several factors when determining your tax residency status.

The concept of tax residency is based mainly on the “permanent place of abode” test and on a day count test involving the days present in New Zealand.

Determining Your Tax Residency Status

The 183 Day Rule

The 183-day rule

Generally, you become a New Zealand tax resident if you are present in New Zealand for more than 183 days during any 12-month period.

The days do not need to be consecutive.

Permanent Place of Abode

Permanent place of abode

Even if you spend considerable time overseas, you may still be considered a New Zealand tax resident if you maintain a permanent place of abode in New Zealand.

This means someone living overseas for several years could still remain a New Zealand tax resident depending on their circumstances.

When do you stop being a New Zealand tax resident?

Becoming a non-resident isn’t as simple as leaving the country.

Generally, you’ll cease being a New Zealand tax resident once:

- you’ve been absent from New Zealand for more than 325 days in any 12-month period, and

- you no longer have a permanent place of abode in New Zealand.

Many people incorrectly assume that moving overseas automatically changes their tax residency.

In reality, each situation needs to be assessed based on your personal circumstances.

Can you be a tax resident of two countries?

Yes. It is possible to be considered a tax resident in both New Zealand and another country.

Where this happens, New Zealand’s Double Tax Agreements (DTAs) help determine which country has the primary taxing rights and can reduce the risk of paying tax twice on the same income.

Professional advice is particularly valuable if you:

- move frequently between countries

- work remotely overseas

- own overseas investments

- receive foreign superannuations

- have business interests in multiple countries

What is a Double Tax Agreement?

Double tax agreements are designed to prevent double taxation, allowing foreign tax credits to offset your NZ tax liability.

New Zealand has a double tax agreement with a number of countries.

These tax agreements cover which country can tax which income source and at what rate.

They also have tiebreaker tests for determining tax residency in dual residency situations.

How Does New Zealand Tax Overseas Income?

If you’re a New Zealand tax resident, you’re generally required to declare worldwide income on your NZ tax return.

Examples may include:

- Salary or wages earned overseas

- Rental income from properties you own overseas

- Interest earned from overseas bank accounts

- Interest you earn from money invested overseas

- Superannuation or pensions from another country

- Foreign dividends

- Overseas business income

In New Zealand, a person’s liability for tax on overseas income in NZ depends on your residency status and any double tax agreements between New Zealand and the source country.

Depending on your circumstances, you may be entitled to foreign tax credits to prevent double taxation where tax has already been paid overseas.

IR1261 Overseas Income Summary

If you receive overseas income, Inland Revenue may require you to complete an IR1261 Overseas Income Summary.

This form helps report foreign income and any overseas tax paid so IRD can determine your New Zealand tax position and calculate any available foreign tax credits.

The information required can vary depending on the type of overseas income you receive.

Professional advice can help ensure the form is completed accurately and that all available tax credits are claimed.

Receiving money from overseas

Receiving money from overseas doesn’t automatically mean you have to pay tax.

Whether tax applies depends on:

- why the money was received

- whether it represents taxable income

- your New Zealand tax residency status

- whether tax has already been paid overseas

For example, transferring your own savings into New Zealand is generally treated differently from receiving overseas employment income or investment income.

Working overseas while living in New Zealand

Many New Zealand residents now work remotely for overseas employers or international clients.

If you remain a New Zealand tax resident, your overseas employment income may still need to be declared in New Zealand, even if tax has already been deducted in another country.

This is one of the most common situations where international tax advice can help avoid double taxation and ensure the correct foreign tax credits are claimed.

Returning to New Zealand after living overseas

Returning to New Zealand often creates new tax obligations.

Depending on your circumstances, you may need to consider:

- your New Zealand tax residency status

- overseas investments

- foreign superannuation

- overseas trusts

- overseas rental properties

- overseas bank accounts

- foreign tax credits

Planning before returning can often reduce future tax complications.

Contact ABA to make an appointment to discuss your situation.

When should you seek international tax advice?

International tax rules are considerably more complex than standard New Zealand tax compliance.

Professional advice is recommended if you:

- are moving overseas

- are returning to New Zealand

- work remotely for an overseas employer

- earn overseas contracting income

- own overseas rental property

- receive foreign superannuation

- have overseas investments

- have become a tax resident of another country

- need assistance with IR1261 reporting

- want to understand your worldwide income obligations

Incorrect reporting can result in penalties or backdated tax. ABA can assist with:

- Income classification

- Currency conversion compliance

- Double tax relief applications

- Overseas tax return reviews

- Foreign Investment Fund (FIF) income

- New Zealand controlled foreign companies

- Undeclared foreign income

- Foreign trusts

Working with an international tax accountant in NZ ensures your overseas income is reported correctly and efficiently.

At ABA Chartered Accountants, we help clients understand their New Zealand tax residency, overseas income obligations and international tax responsibilities, ensuring they remain compliant while avoiding unnecessary tax where possible.

Need advice about your tax residency or overseas income?

If you’re unsure whether you’re a New Zealand tax resident, need help declaring overseas income or want advice before moving to or from New Zealand, our experienced team can help.

We’ll explain your obligations in plain English, identify any available tax relief and ensure you’re meeting your Inland Revenue requirements with confidence.

schedule a meeting Give Us A callABA Chartered Accountants Provide International Tax Advice

Do any of these situations apply to you?

NZ Tax Resident Working Overseas

If you’re working overseas but remain a New Zealand tax resident, you’re required to:

- Report all foreign-sourced income

- Claim any allowable foreign tax credits

- Disclose overseas bank accounts, pensions or trusts (if applicable)

Our team specialises in overseas tax advice for expats and Kiwis abroad. We work closely with you to manage NZ compliance while optimising tax efficiency across borders.

Yacht Crew Tax Specialist

If you’re part of the superyacht crew or working on international vessels, you may assume you’re exempt from NZ tax – but that’s not always the case.

ABA are yacht crew tax specialists, helping seafarers understand their tax obligations.

We offer practical advice on tax residency, foreign income reporting, and student loan repayments for yachties.

Contact ABA for advice on your specific situation.

Overseas Rental Tax Returns NZ

Do you own rental property overseas? If you’re an NZ tax resident, you must include this income in your tax return.

ABA provides full support for:

- Overseas rental tax returns (NZ)

- Deductible expenses and depreciation schedules

- Exchange rate conversion compliance

- Foreign tax credit claims

Contact us for assistance with your overseas rental property tax returns.

Filing Tax Returns for Overseas Income

If you receive income from overseas during the year, you are generally required to file an Individual Income Tax Return (IR3) with Inland Revenue at the end of the financial year. This applies even if you arrived in New Zealand partway through the year or spent time living abroad.

As part of your return, you must complete an Overseas Income Summary (IR1261), detailing the types of foreign income earned and any overseas tax paid. These amounts must be converted to New Zealand dollars and reported correctly to ensure IRD can assess whether any foreign tax credits are available.

If you were a New Zealand tax resident for only part of the year, you’ll need to separate your income into the period you were a resident and the period you were not. This ensures that income is taxed according to your correct residency status.

Key dates and filing requirements:

- The New Zealand tax year runs from 1 April to 31 March.

- Returns are generally due by 7 July, unless you work with a tax agent who has an extension of time.

Not sure how your foreign income is taxed or which forms apply to your situation? Contact ABA, we can assist you.

FAQ: Tax Residency and Overseas Income NZ

What is tax residency?

Tax residency determines whether you’re taxed on worldwide income in NZ or only on income sourced within NZ. It’s based on your presence in NZ and the concept of a permanent place of abode.

What is a New Zealand tax resident?

A New Zealand tax resident is someone who meets Inland Revenue’s tax residency tests, including the 183-day rule or the permanent place of abode test. Tax residents are generally taxed on their worldwide income.

How does IRD determine tax residency?

Inland Revenue determines your tax residency by looking at your personal circumstances and applying two main tests: the 183-day rule and the permanent place of abode test. If you’ve been in New Zealand for more than 183 days in any 12-month period, you’ll generally become a New Zealand tax resident.

Even if you’ve spent significant time overseas, you may still be considered a tax resident if you maintain a permanent place of abode in New Zealand. Because every situation is different, it’s important to seek professional advice if you’re unsure of your tax residency status.

What is the 183-day rule?

If you spend more than 183 days in New Zealand during any 12-month period, you will generally become a New Zealand tax resident for tax purposes.

What is a permanent place of abode?

A permanent place of abode refers to your ongoing connection with New Zealand. Inland Revenue considers factors such as your home, family, economic interests and social ties when determining whether you remain a New Zealand tax resident.

What is a non-resident for tax purposes in New Zealand?

You may be a non-resident if you’ve been out of NZ for more than 325 days in a 12-month period and have no enduring ties to NZ – But this needs to be assessed carefully.

When do I stop being a New Zealand tax resident?

Generally, you’ll stop being a New Zealand tax resident once you’ve been outside New Zealand for more than 325 days in a 12-month period and no longer have a permanent place of abode here.

Can I be a tax resident of two countries?

Yes. It is possible to be a tax resident in more than one country. Double Tax Agreements help determine which country has primary taxing rights in these situations.

What is a Double Tax Agreement (DTA)?

A Double Tax Agreement (DTA) is an agreement between New Zealand and another country that helps prevent the same income from being taxed twice. DTAs determine which country has the primary right to tax certain types of income and may allow you to claim foreign tax credits or exemptions. They are particularly important for people who work overseas, own foreign investments or earn income in more than one country.

Does New Zealand tax worldwide income?

If you’re a New Zealand tax resident, you’ll generally need to declare your worldwide income to Inland Revenue. This includes income earned both in New Zealand and overseas, such as foreign salary and wages, rental income, investment income and some overseas pensions. If you’ve already paid tax on that income in another country, you may be entitled to claim foreign tax credits to reduce the amount of tax payable in New Zealand.

Do New Zealand tax residents pay tax on overseas income?

Generally, yes. New Zealand tax residents are required to declare their worldwide income, although foreign tax credits or Double Tax Agreements may reduce double taxation.

What counts as overseas income?

Overseas income can include foreign wages, overseas business income, rental income from overseas property, foreign pensions, dividends, interest and some investment income.

Do I have to pay tax if I receive money from overseas?

Not necessarily. Whether tax applies depends on why you received the money, whether it represents taxable income and your tax residency status.

Do I pay tax on money transferred from overseas to New Zealand?

Simply transferring money from overseas to New Zealand doesn’t automatically mean you’ll have to pay tax. Whether tax applies depends on the source of the funds and your tax residency status.

For example, transferring your own savings is generally not taxable, while overseas employment income, investment income or rental income may need to be declared if you’re a New Zealand tax resident. If you’re unsure whether funds transferred from overseas need to be reported, it’s worth seeking professional advice before lodging your tax return.

What is the IR1261 Overseas Income Summary?

The IR1261 is an Inland Revenue form used to report overseas income and foreign tax paid so the correct New Zealand tax treatment can be determined.

Am I a tax resident of NZ?

If you’ve spent 183+ days in NZ in a 12-month period, or have a home or family here, you may be a tax resident. ABA can review your case to confirm.

Should I get professional international tax advice?

If you earn overseas income, are moving between countries, own overseas investments or are unsure about your tax residency status, professional advice can help you remain compliant while avoiding unnecessary tax.

What is the tax on student loans when overseas (NZ)?

If you’re living overseas and have a NZ student loan, you’re generally required to make fixed repayments. Late or non-payment incurs interest and penalties. ABA can help manage your obligations.

Can I claim tax back on overseas donations (NZ)?

Only donations made to approved NZ charities are eligible for tax credits. Donations to overseas organisations generally don’t qualify.

Do I pay tax on money transferred from overseas to New Zealand?

Not necessarily. It depends on the source of the funds. Gifts and inheritances may not be taxable, but foreign income is. ABA can advise based on your situation.

How are overseas bonds taxed in NZ?

Foreign bonds may be subject to NZ’s Foreign Investment Fund (FIF) rules. These rules can be complex and depend on the value and nature of your investments.

What our clients say…

Lets talk